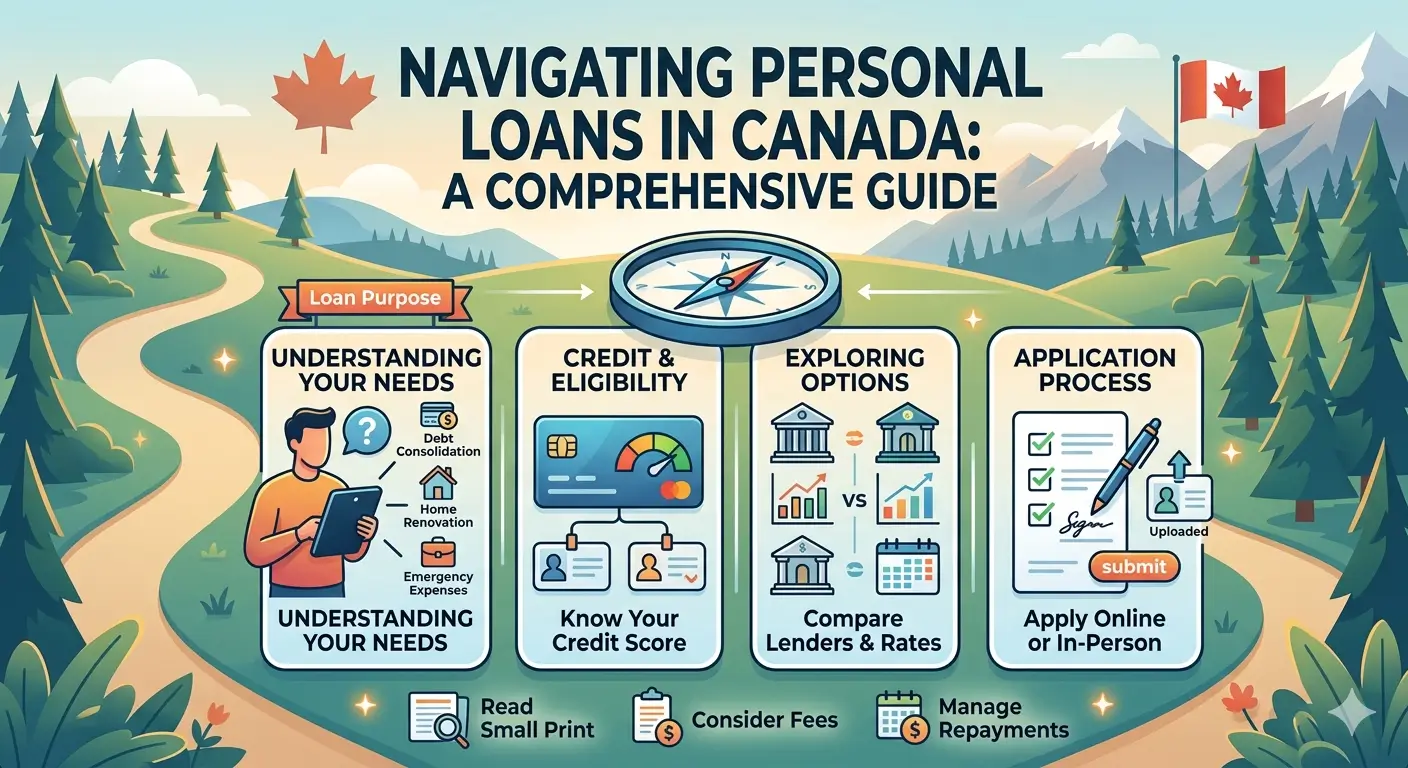

Personal loans are one of the most flexible financial tools available to Canadians. Whether you are consolidating debt, covering unexpected expenses, funding a major purchase, or managing a life transition, a personal loan can provide structured, predictable financing with clear repayment terms.

But the Canadian lending landscape is complex. Banks, credit unions, online lenders, and alternative financing companies all offer different products — each with its own rates, requirements, and approval criteria. This guide breaks down everything you need to know so you can make an informed, confident decision.

1. Unsecured Personal Loans

These are the most common. They do not require collateral and are approved based on:

• Credit score

• Income stability

• Debt‑to‑income ratio

• Employment history

Best for: Everyday borrowing, debt consolidation, emergency expenses, or general financial needs.

2. Secured Personal Loans

Secured personal loans require collateral such as a vehicle, savings account, or other asset. Because the lender has security, interest rates may be lower.

Best for: Borrowers with lower credit scores or those seeking better rates.

3. Debt Consolidation Loans

Designed to combine multiple debts into one manageable payment. This can simplify budgeting and may reduce overall interest costs.

Best for: Canadians juggling credit card balances, payday loans, or multiple high‑interest debts.

4. Personal Lines of Credit

A revolving credit product that allows you to borrow as needed, similar to a credit card but often with lower interest rates.

Best for: Ongoing or unpredictable expenses.

5. Emergency or Short‑Term Loans

These loans provide quick access to funds but may come with higher rates. It’s important to compare options carefully.

Best for: Urgent, time‑sensitive financial needs

Interest rates vary widely depending on:

• Credit score

• Income and employment stability

• Loan amount

• Loan term

• Whether the loan is secured or unsecured

• Lender type (bank vs. online lender vs. alternative lender)

Typical Rate Ranges

• Excellent credit: Lower rates, often competitive with bank products

• Good credit: Moderate rates

• Fair or poor credit: Higher rates, but still structured and predictable

Canada Wide Credit emphasizes transparency and responsible borrowing, helping you compare options without pressure.

While each lender has its own criteria, most look for:

• Proof of Canadian residency

• Government‑issued ID

• Proof of income (pay stubs, bank statements, or tax documents)

• Employment verification

• Credit history

• Banking information for deposits and payments

Some lenders also consider alternative data such as cash‑flow patterns or length of employment.

The application process typically includes:

1. Assessing Your Needs

Determine how much you need to borrow and what repayment term fits your budget.

2. Checking Your Credit

Understanding your credit score helps you anticipate your approval odds and potential rates.

3. Comparing Lenders

Look at:

• Rates

• Fees

• Terms

• Funding speed

• Customer reviews

• Transparency

4. Submitting Your Application

Most lenders allow online applications with quick decisions.

5. Reviewing Your Loan Agreement

Before accepting, review:

• Interest rate

• Total cost of borrowing

• Payment schedule

• Prepayment options

• Fees or penalties

6. Receiving Your Funds

Funds are typically deposited directly into your bank account.

Personal loans can help build or rebuild credit when managed responsibly.

Positive impacts:

• On‑time payments improve your score

• A personal loan adds credit mix

• Paying down high‑interest debt can reduce credit utilization

Potential negative impacts:

• Missed payments harm your score

• Taking on too much debt can increase financial stress

Canada Wide Credit encourages responsible borrowing and provides guidance to help you stay on track.

The application process typically includes:

1. Assessing Your Needs

Determine how much you need to borrow and what repayment term fits your budget.

2. Checking Your Credit

Understanding your credit score helps you anticipate your approval odds and potential rates.

3. Comparing Lenders

Look at:

• Rates

• Fees

• Terms

• Funding speed

• Customer reviews

• Transparency

4. Submitting Your Application

Most lenders allow online applications with quick decisions.

5. Reviewing Your Loan Agreement

Before accepting, review:

• Interest rate

• Total cost of borrowing

• Payment schedule

• Prepayment options

• Fees or penalties

6. Receiving Your Funds

Funds are typically deposited directly into your bank account.

To make the best decision:

• Compare multiple lenders

• Look for transparent terms

• Avoid products with unclear fees

• Choose a repayment term that fits your budget

• Consider secured options if you want lower rates

• Avoid borrowing more than you need

A personal loan may not be ideal if:

• You cannot comfortably afford the monthly payments

• You have access to lower‑cost alternatives

• You are using the loan for non‑essential spending

Responsible borrowing is key to long‑term financial health

Canada Wide Credit’s network provides:

• A supportive, non‑judgmental experience

• Access to a wide network of lenders

• Transparent information

• No‑pressure guidance

• Options for all credit situations

• A simple, mobile‑friendly process

Our goal is to help Canadians make informed, confident financial decisions

If you’re considering a personal loan, review our full guide to Personal Loans in Canada for clear, Canadian‑focused advice on rates, qualification, and choosing the right lender.

1. What can I use a personal loan for in Canada?

Personal loans can be used for many purposes, including debt consolidation, emergency expenses, home repairs, medical costs, moving expenses, or major purchases. Lenders typically allow flexible use as long as the loan is managed responsibly.

2. How much can I borrow with a personal loan?

Loan amounts vary by lender, credit profile, income, and whether the loan is secured or unsecured. Many lenders offer personal loans ranging from a few thousand dollars up to $50,000 or more.

3. How long are personal loan terms in Canada?

Most personal loans offer repayment terms between 12 and 60 months. Longer terms reduce monthly payments but may increase total interest costs.

4. Are there fees associated with personal loans?

Some lenders may charge administrative fees, origination fees, or early repayment fees. Reviewing the loan agreement carefully helps ensure you understand the total cost of borrowing.

5. How fast can I receive funds after approval?

Funding times vary by lender. Some online lenders offer same‑day or next‑day deposits, while banks and credit unions may take a few business days.

6. Is a personal loan better than using a credit card?

A personal loan may offer lower interest rates and predictable payments, making it a better option for larger expenses or debt consolidation. Credit cards may be more flexible for smaller or ongoing purchases.