How bad credit debt consolidation loans work in Canada, when they help, and what to watch out for.

More Canadians with damaged credit are searching for ways to avoid bankruptcy while still getting their debt under control. A bad credit consolidation loan can sound like a lifeline, but it comes with real trade-offs. This guide explains how it works in Canada, when it helps, and when to be cautious.

A bad credit consolidation loan is an unsecured personal loan (or sometimes a secured loan) used to pay off multiple existing debts, such as credit cards, lines of credit, and payday loans. Instead of juggling several payments, you make a single monthly payment to one lender, usually at a fixed interest rate.

For Canadians with low credit scores, these loans are typically offered by alternative lenders, online lenders, and some credit unions. The interest rate is usually higher than prime personal loans, but still lower than credit card or payday loan rates. The goal is to simplify payments and reduce the overall cost of debt over time.

Because the loan is designed for borrowers with late payments, collections, or past delinquencies, approval criteria are more flexible. Lenders may focus on income stability, debt-to-income ratio, and recent payment behaviour rather than just the credit score itself.

Understanding the process helps you decide whether this option fits your situation.

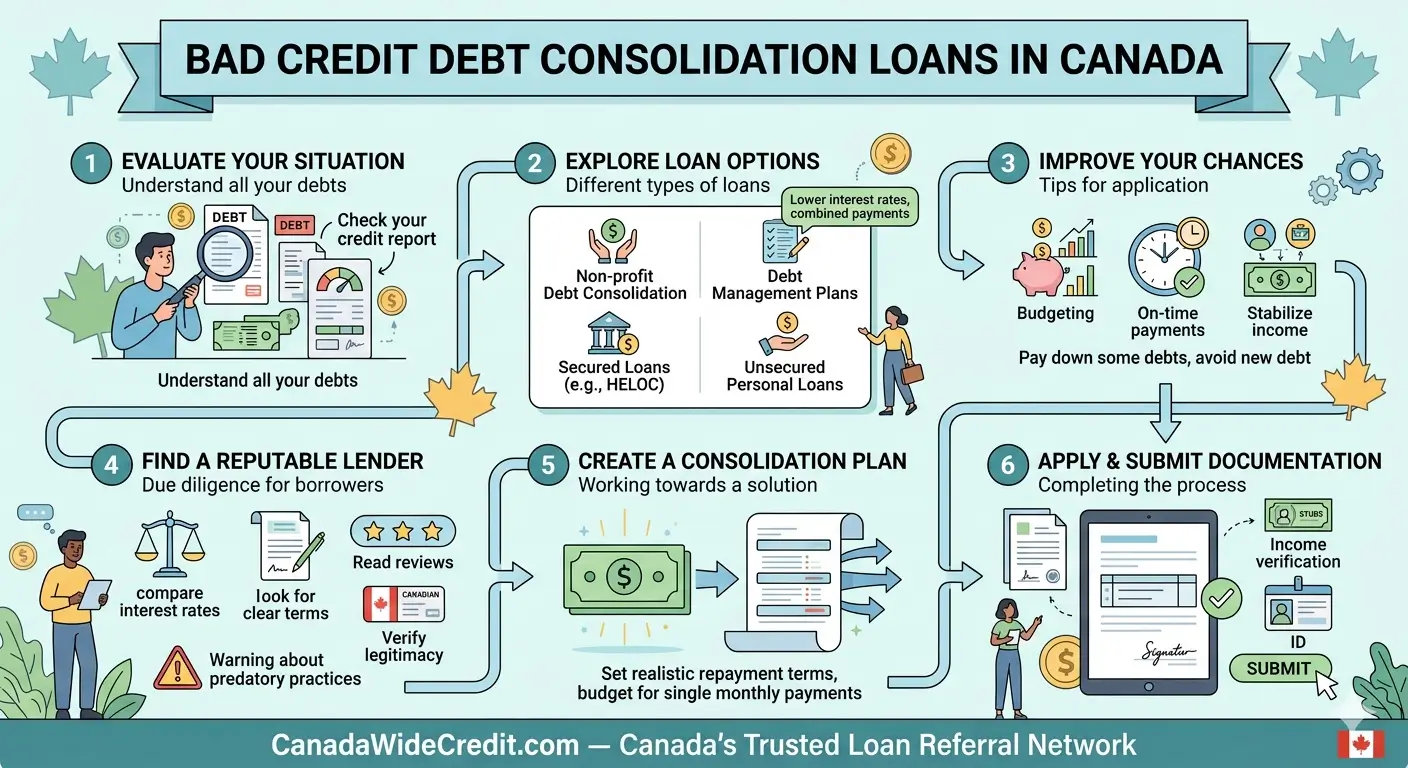

You start by listing all your unsecured debts: credit cards, lines of credit, payday loans, buy-now-pay-later balances, and overdue bills. The total amount, interest rates, and minimum payments help determine how large a consolidation loan you would need.

Even with bad credit, lenders will review your credit report, income, and monthly obligations. Many bad credit lenders in Canada accept scores in the low 600s or even high 500s, provided your income can support the new payment. Some use soft checks at the pre-qualification stage.

Instead of applying randomly, it is better to focus on lenders that explicitly work with bad credit borrowers. A platform that compares bad credit loans in Canada can help you avoid repeated hard checks and mismatched offers.

If approved, the lender either deposits the funds into your account or pays your creditors directly. Your old balances are cleared, and you now have one new loan with a fixed payment schedule, usually over two to five years.

The real benefit comes from making every payment on time and avoiding new high-interest debt. Over time, consistent payments can help rebuild your credit profile, while missed payments can make things worse than before.

In Canada, bad credit consolidation loans are offered by a mix of banks, credit unions, online lenders, and finance companies. Big banks tend to reserve their best rates for higher credit scores, so many bad credit borrowers turn to alternative lenders that specialise in higher-risk profiles.

Provincial regulations cap interest rates and set rules for payday loans, but consolidation loans are usually governed by federal criminal interest rate limits and consumer protection laws. Even so, rates can still be high compared to prime products, so it is important to compare offers carefully.

Credit scores in Canada typically range from 300 to 900. Many lenders consider scores below 660 as “non-prime” or “subprime.” If your score is in this range, you may still qualify for a consolidation loan, but the rate will reflect the perceived risk. Some borrowers use a secured consolidation loan backed by a vehicle or home equity to access lower rates, but that increases the risk of losing the asset if payments are missed.

Insolvency options—like consumer proposals and bankruptcies—are governed by federal law and administered by Licensed Insolvency Trustees. Rising insolvency chatter and social media content about “avoiding bankruptcy” are pushing more Canadians to explore consolidation loans as a last attempt before formal insolvency.

Because bad credit consolidation loans are heavily marketed, it is easy to misunderstand what they can and cannot do.

No. Consolidation itself does not magically repair your credit. Your score may dip slightly after the new inquiry and account are added. Over time, however, making on-time payments and reducing overall debt can help improve your score.

No. A consolidation loan is a new loan you must fully repay, with interest. A consumer proposal is a legal process that can reduce the amount you owe and stops interest, but it has a stronger negative impact on your credit and stays on your report for years after completion.

Not necessarily. Some lenders blur the line between instalment loans and payday-style products, with high fees and aggressive terms. Always read the full cost of borrowing, check for provincial licensing where applicable, and avoid lenders that pressure you to sign immediately.

Yes, some lenders allow you to consolidate payday loans into a longer-term instalment loan. This can lower your monthly payment and reduce the effective interest cost, but only if you stop using payday loans going forward.

A bad credit consolidation loan can be helpful, but it is not the right tool for every situation.

It may be worth considering when your total debt is still manageable, you have stable income, and the consolidation loan offers a lower blended interest rate than your current debts. If the new payment fits comfortably within your budget and you are committed to not reusing old credit cards, consolidation can simplify your finances and support gradual credit rebuilding.

If your debt is already unmanageable—missed payments, collection calls, and no realistic way to afford even a reduced payment—a consolidation loan might only delay the inevitable. In those cases, speaking with a non-profit credit counsellor or Licensed Insolvency Trustee about a consumer proposal or other options may be more appropriate.

Be cautious if the lender charges large upfront fees, pushes you to borrow more than you need, or suggests you lie on your application. Also be wary of offers that sound like “no credit check” but hide extremely high interest rates and penalties in the fine print.

Depending on your situation, you might explore a debt management program through a credit counselling agency, a secured consolidation loan using a vehicle or home equity, or, in more serious cases, a consumer proposal. Comparing multiple bad credit loan options in Canada can help you see where consolidation fits among these choices.

If you are weighing a bad credit consolidation loan against other borrowing options, start with the full overview of lenders, rates, and approval criteria in this guide: Bad Credit Loans: Fast, Transparent, Financing Options. It explains how different bad credit loan types compare and how to choose the right path for your situation.

Not always. You need to compare the total cost of the new loan—including interest and fees—against what you would pay if you kept your current debts and made an aggressive repayment plan. A longer term with a lower payment can still cost more overall.

Some online lenders can provide a decision within minutes and funding within one or two business days. Others, especially credit unions, may take longer and require more documentation. Timing depends on the lender, your profile, and how quickly you submit documents.

Some lenders may approve you without a co-signer, while others might require one to offset risk. A strong co-signer can improve your chances and potentially lower your rate, but they become fully responsible if you miss payments.

Approval is more difficult if you are in an active proposal, but some specialised lenders may consider it. In many cases, it is better to complete the proposal first and then focus on rebuilding credit with smaller, more manageable products.

A bad credit consolidation loan can be a useful tool for Canadians trying to avoid bankruptcy and regain control of their debt, but it is not a magic fix. Compare offers carefully, understand the total cost, and be honest about your budget before committing to a new loan.

Compare your loan options: Compare Tool

Competitive rates from trusted Canadian lenders! Get behind the wheel in just a few clicks.

Competitive rates from trusted Canadian lenders! Get behind the wheel in just a few clicks.

* Calculations are estimates for educational purposes only. Actual interest rates, fees, and approvals are determined solely by lending partners based on your personal credit profile.